Sales tax nexus is the connection between your business and a state that creates a requirement to collect and remit sales tax from customers in that state.

While this used to depend solely on having a physical office or warehouse, modern rules now include many other forms of nexus, like economic nexus. Economic nexus is established when a business reaches a specific sales volume or transaction count in a state, often $100,000 in gross sales or 200 separate transactions, and in many cases, both.

This article will walk you through many high-risk types of nexus, explain how trailing nexus works, and provide a framework for deciding exactly when to register.

There are many different types of nexus. Each has its own set of rules, and often each state has its own interpretation of those rules.

For example, if you send a team member to a trade show in California for just one day, you have triggered physical nexus and must collect sales tax. But in Arizona, you can typically attend for up to two days without triggering sales tax nexus.

It is also important to note that a business can trigger several types of nexus at the same time. For example, you might have physical presence in a state because of a remote employee, while simultaneously triggering economic nexus by crossing their sales threshold.

Here's a quick breakdown of the different types of nexus, followed by a deep dive on each.

|

Nexus Type |

Definition |

Common Trigger |

|

Based on tangible assets or people. |

Having an office, warehouse, or remote employee in a state. |

|

|

Based on the volume of business you do. |

Reaching a specific dollar amount (e.g., $100k) or transaction count. |

|

|

Created through relationships with other businesses. |

Using a local business to help sell or deliver your products. |

|

|

Triggered by online referrals. |

Paying a local website a commission for sending customers to you. |

|

|

Marketplace activities that could trigger an obligation. |

Selling through Amazon, Walmart, or Etsy (where they collect for you). |

Physical presence is the original form of sales tax nexus. It applies when your business has a tangible presence in a state.

While this includes obvious things like offices or storefronts, it sometimes also counts for things like:

Economic nexus is triggered by your sales activity within a state.

Most states have set an economic threshold, commonly $100,000 in gross sales or 200 separate transactions. Others have higher limits like $200,000 to $500,000.

While this is often measured over a calendar year, many states use different 'lookback periods,' such as a rolling 12-month window.

Note: If you sell in multiple states, you should monitor your sales volumes and transaction amounts in each state to track when you are getting close to a threshold. A sudden spike in sales could create new sales tax responsibilities almost overnight.

Affiliate nexus happens when an out-of-state business has a relationship with an in-state person or company that brings in sales.

For example, say you run an online outdoor gear brand based in Colorado. If a popular hiking guide in Utah hands out your discount cards, Utah sees them as your in-state affiliate. That relationship may require you to collect sales tax in Utah.

Here are the most common ways businesses establish affiliate nexus:

Click-through nexus happens when your business uses out-of-state digital referrals.

If you pay a commission to an influencer, blogger, or website owner based in another state for sending customers to your site via a link, that state requires you to collect sales tax.

Here is what usually triggers a click-through nexus:

If you sell your products on major websites like Amazon, eBay, or Etsy, the law usually requires these platforms to collect and file the sales tax for you. This is known as marketplace facilitator laws, and just like most tax regulations, the specific rules and expectations vary by state.

For example, if your Texas-based business sells custom mugs on Etsy, Etsy collects and remits the sales tax for all your buyers' states on the platform.

This takes a major operational load off your plate. However, your marketplace activity still creates new obligations. Here is what it can affect:

Trailing nexus comes into play once your nexus activity has stopped in a state. Instead of immediately ending your obligations, it requires you to continue collecting and remitting sales tax on any taxable sales you make in that state for a set period, often a full calendar year. You would only file $0 returns if you had absolutely no sales during that time.

For example, if you let go of your only remote employee in Washington state in January, you might still have to collect Washington sales tax for the rest of that year and the entire following calendar year. Keep in mind that this only applies if the remote employee was the only thing creating nexus in that state.

Trailing nexus exists because states use structured, administrable rules for tax obligations that don’t immediately shut off when your activity stops.

It’s also best to avoid rushing to cancel your sales tax permits because it can cause a few problems, like:

You have nexus once you meet one of the nexus thresholds within a state. That’s when you should apply for a sales tax permit in that state. Once you have the permit, you should start collecting and remitting sales tax.

However, it's important to note that the exact registration timeline depends on the state and the type of nexus you triggered.

For example, some states give you a 60-day grace period to register after you cross an economic nexus threshold, but physical presence typically has no grace period at all. So, while crossing a threshold doesn't necessarily mean you have to register that immediate moment, it definitely could.

Once you have the permit, you should start collecting and remitting sales tax.

Note: It is illegal to collect sales tax without being officially registered with the state.

The states are not going to send you an email or call you to let you know when you have nexus. It’s up to you and your team to know when you have nexus and when to register for a sales tax permit in a state.

If you're attempting to manage this alone, follow these tips. This list is not exhaustive (we know that activities like attending trade shows or conferences can impact nexus, among many other activities), but it will help you begin your assessment:

When checking if you've hit a state's threshold, remember that states usually count your gross sales, which include exempt or non-taxable items. However, there is no one-size-fits-all rule. What actually counts toward the limit that triggers your legal obligation to register depends entirely on the state. Some states include marketplace or wholesale sales in your total, while others do not.

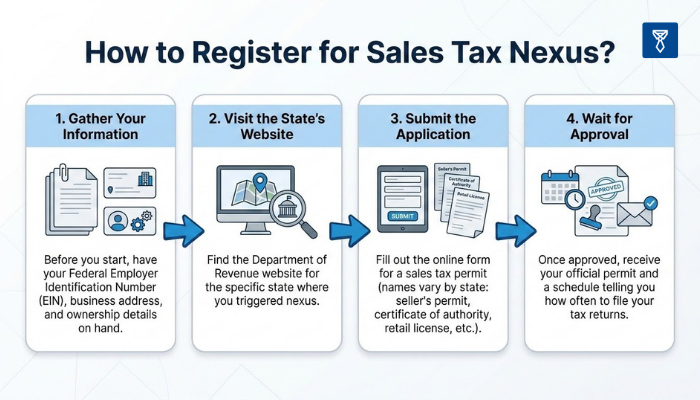

Once you know which states you need to register in, the actual registration process is a series of administrative steps. While not exactly the same for all 50 states, they often follow this general format:

Doing this for one state is manageable, but if you have nexus in multiple states, the paperwork multiplies quickly. If you want to offload the compliance burden completely, a managed service like TaxValet handles all the registrations, monthly filings, and nexus monitoring for you.

Managing sales tax isn’t easy. Between tracking physical and economic triggers, dodging the use tax pitfalls, and monitoring new laws, staying compliant demands specialized expertise and significant internal resources.

But it doesn't have to be you or your finance team’s job.

At TaxValet, we replace the burden of compliance with certainty. With a dedicated team of experts, your sales tax is:

VAT (Value Added Tax) is a national-level tax collected at every stage of the supply chain in many countries outside the U.S. In contrast, U.S. sales tax is decentralized across states and thousands of local jurisdictions. It is generally a single-stage tax charged only to the final consumer at the point of sale.

While sales tax laws contain a lot of nuance and grey area, nexus generally falls into a few primary buckets. The most impactful types are physical presence, economic, affiliate, and click-through nexus. Each has its own specific triggers, ranging from having a remote employee to hitting a specific revenue threshold in a calendar year.

Exemptions vary by state, but they generally fall into three categories: purchaser-based (such as government agencies and non-profits), item-based (such as essential groceries or prescription medicine in some states), and use-based (such as raw materials purchased for manufacturing or items bought for resale).

Neither. The United States uses a sales and use tax system governed independently by each state.

{kind=link}