Economic nexus is established by state laws that require your business to collect and pay sales tax based solely on your sales revenue, number of transactions, or both.

Before the 2018 South Dakota v. Wayfair, Inc. Supreme Court ruling, states only taxed businesses with physical presence in a state, like storefronts or warehouses. Today, selling a certain amount of goods or services online in a state is enough to trigger this sales tax obligation.

This guide covers economic nexus thresholds, your next steps when crossing them, the risks of non-compliance, state-by-state specifics, and state measurement periods.

An economic nexus threshold is a specific revenue limit or transaction count set by a state. Once your business crosses this limit, it triggers a legal obligation to register, collect, and remit sales tax.

The most common nexus threshold across the states is $100,000 in annual sales or 200 separate transactions, and sometimes both. However, some states often set higher limits, like California and Texas, which both have a $500,000 threshold with no transaction count.

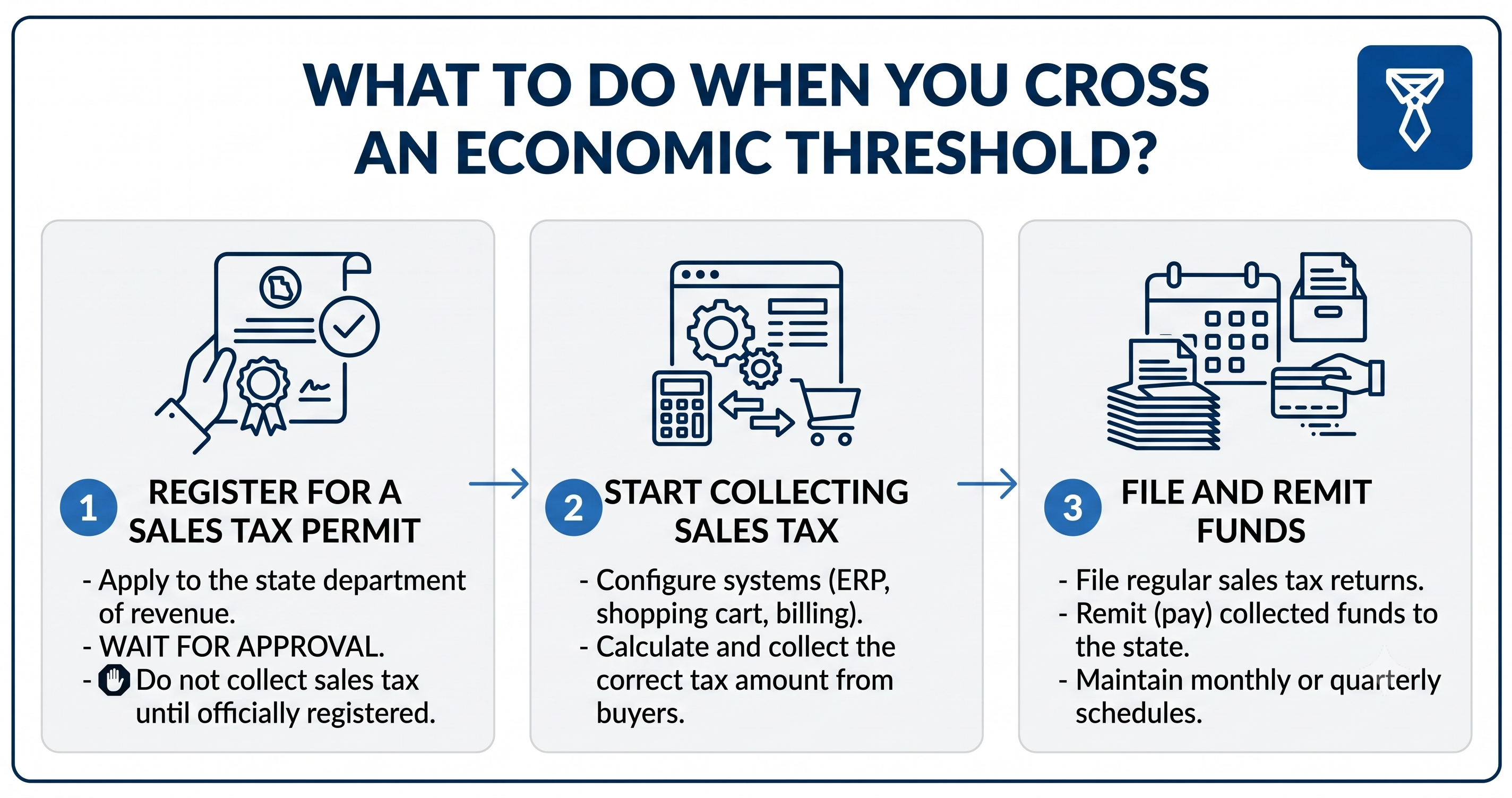

Here is exactly what you need to do when your business hits a state's economic nexus threshold:

If your business crosses a nexus threshold but fails to register and collect sales tax, that state can audit your business. In most cases, the state will demand all the taxes you should have collected from your past customers, along with interest and penalties.

If you didn't collect the sales tax at the time of the sale, you will have to pay those back taxes entirely out of your own pocket

You also have to be careful with marketplace platforms like Amazon and Etsy:

Every state sets its own economic nexus thresholds.

To help, here is a quick overview of how the states are currently grouped based on their limits.

These states have higher dollar nexus limits, making it much easier for scaling enterprises to avoid having to register immediately.

These states set nexus thresholds based solely on your sales revenue. It doesn't matter if you make 10 large sales or 10,000 small ones; if your total revenue hits the dollar limit, you have to register.

A measurement period (often called a lookback period) is the timeframe a state uses to calculate your past sales. This means the state only counts the sales within that defined period when they measure if you’ve hit a threshold.

However, not every state uses the same timeline.

Right now, states generally fall into one of four measurement categories:

In these states, your requirement to collect tax in the current year is based entirely on what you sold between January 1 and December 31 of the previous year. For example, if you crossed the threshold in 2025, your legal obligation to collect tax began on January 1, 2026.

Tip: Review your final gross sales for the previous calendar year. If you hit the limit in one of these states, you need a permit for the current year.

This is the most common measurement period. Nexus is triggered the moment you cross the threshold in the current year, OR if you crossed it anytime during the previous year.

Tip: Monitor your sales in real-time. A sudden spike in sales could trigger nexus.

These states look at the immediate 12 months prior to today when measuring if you’ve triggered nexus.

Tip: Check your sales for the last 365 days at the end of every month. A sudden spike in holiday sales could trigger an obligation, even if your overall yearly total was low.

These few states use specific date ranges to measure your sales:

Managing economic nexus thresholds, complex measurement periods, and differing state laws is a big operational burden for your finance team.

Let TaxValet operate as your Fractional Sales Tax Department instead.

You get a truly end-to-end service that handles your entire sales tax compliance workload (including nexus), eliminates costly sales tax risks, and operates with accountability.

You focus on high-level strategy, and TaxValet’s expert team will make sure your sales tax is handled perfectly.

Yes. US states don’t care where your headquarters are. If a foreign company hits a state's revenue or transaction limit, they must register and collect sales tax just like a US-based seller.

In many states, yes. As a general rule, most states base thresholds on your gross sales, which include tax-exempt, wholesale, and non-taxable transactions. However, there are plenty of states that only look at your taxable sales. If a state does use gross sales, crossing the limit means you must register and file "zero-dollar" returns even if you owe zero actual tax.

It depends on the state. Many states allow you to deregister as soon as your sales drop below the threshold and you no longer have economic nexus. However, you must watch out for states with trailing nexus rules. In these specific states, you’re legally required to keep your permit active and continue collecting tax for a set period (like the remainder of the calendar year) even after your sales decrease. Canceling your permit too early in a trailing-nexus state can trigger penalties.

Yes. The taxability of SaaS and digital products varies by state. However, even in states that don’t tax SaaS, the revenue from those sales usually still counts toward your gross sales threshold, which can trigger a registration requirement.

Hidden sales tax liabilities routinely delay deals or slash valuations. Buyers will run their own nexus checks. If they find historical exposure, they will either require you to escrow funds to cover the back taxes or walk away entirely to avoid inheriting the risk.

{kind=link}